Ludwig von Mises / (@CatalystVoices, 2021)

💰Financial History Piece: The Federal Reserve & WTF Happened in 1971?

Ever since “The Everything Code” I truly started the think about ways to capitalize on both The Liquidity Cycle & The Business Cycle. I wanted to see if I could identify patterns and/or trends. To identify “what is happening” rather than “what i want and/or i think will happen.” What is happening is this (see figure(s) below).

[Before I share, I’d like to reiterate that: NONE OF THIS IS FINANCIAL ADVICE & FOR ENTERTAINMENT/INFORMATIONAL PURPOSES ONLY. WHAT I DECIDE TO SHARE MEETS MY PERSONAL NEEDS & SITUATION & IS NOT ONE-SIZE FITS ALL ADVICE. IT IS ADVISED YOU DO YOUR OWN DUE DILIGENCE, SEEK A FINANCIAL ADVISOR FOR PERSONAL FINANCIAL ADVICE THAT MEET YOUR OWN PERSONAL NEEDS]. Now, we have this disclaimer out the way, lets begin…

Now, I understand the fundamentals of Bitcoin, I love it, & I truly think it is the future. Having stated this, I should also be extremely clear that I am NOT a Bitcoin maximalist, where I place 100% of my capital into it, even if it is the highest culmulative performing asset over the past decade. I am a believer of “diversifying, but with conviction," meaning that my portfolio consists of only assets that I understand, which are very few, but it isn’t just one.

Because of “The Everything Code,” it really got me thinking about how to diversify within my themes, some now taking higher precedence than others. By acknowledging humanity’s current situation, reflecting on the state of our future existence, & trying to makes sense of it all through the lens of economic history, I am beginning to understand our current system. I am of the opinion that central banks & the entire banking sector, as they have operated since the Great Financial Crisis (2008), feel in many ways like a giant ponzi scheme. While it technically (by definition) isn’t one, it sure does feel like it at times. By studying economic history and reaching such conclusions, has grown my distrust of central authority, which in turn has led me to adopt a more Austrian economic perspective in practice. My economic belief system is physical hard assets > paper assets, because physical hard assets can’t be manipulated like paper assets can.

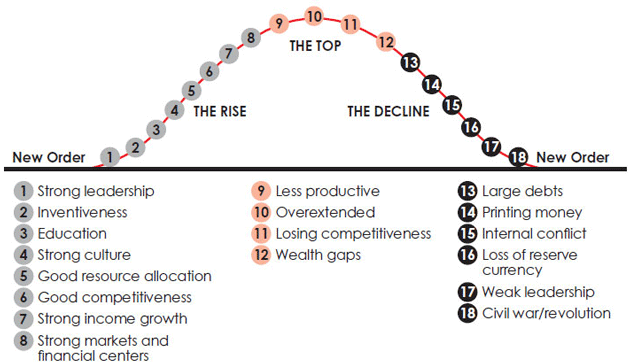

As the world faces consistent evolution & change, historically, humanity’s values & principles run parallel to that change. Through the peaks and valleys of societal influences & changing world orders, it all centers around one thing, cyclicality. Cycles start & finish at changes in “order.” An “order” can refer to internal orders, such as constitutions that govern within countries, or world orders, such as treaties that govern relations between countries. But history has demonstrated that changes in either internal or world orders often require conflict. While such conflicts can be non-violent in nature, the likelihood is higher for more violent measures, such as war. War for territory, war on freedoms, and/or war on money.

When observing the last 10 most powerful empires—the United States of America, British, Dutch, Spanish, German, French, Indian, Japanese, Russian, and Ottoman Empires—as well as the last three reserve currencies (the French Franc from 1720 to 1815, the British Pound from 1815 to 1920, & the U.S. Dollar from 1921 to the present) (Midas Gold Group, 2023), history shows us that wars often occur at monetary inflection points. These points reflect the cyclical nature of money, which alternates between periods of prosperity & periods of debt and destruction (see figure below).

For even greater clarity…

Now that I’ve given a preview, I’d like to take this moment to spotlight, The Federal Reserve, & the critical role it has played since it’s inauguration on December 23rd, 1913.

See, the creation of the Federal Reserve was seen to the masses as peaceful & prosperous (“The Rise”). Fast-forward to 2024 (111 years later), it is everything BUT peaceful & prosperous. IMO (in my opinion), The Federal Reserve is the most powerful & violent institution for the prosperity of humanity in human history. The primary function of the Federal Reserve is to manipulate (aka “manage”) money through two main tools: 1) monetary policy (which involves controlling interest rates & the total money supply) & fiscal policy (which encompasses taxes and government spending).

As of this writing, we are transitioning from a focus on monetary policy to fiscal policy. Why is this problematic? It is problematic because manipulation by a single entity distorts economic reality. Actions by the Federal Reserve create something known as the “Cantillon Effect,” which effectively distributes money (liquidity) throughout the economy, unevenly. This effect disproportionately benefits those who own the assets compared to those who do not (see explainer video below)(River, 2024). To put it simply, today, we are operating in an unfair system that is equitable for a few, rather than the many.

What makes this game so dangerous? The danger lies within how it was initially created, & facing consequences such as losing “the free market”. In a free market, societal activity organically regulates itself. This regulation was all thanks to “the gold standard”. A standard that saw gold as money. A hard to produce scarce asset, that was hard to manipulate.

Before the Federal Reserve, & really up until 1971 (when gold was officially taken off of the “gold standard” by President Richard M. Nixon), the monetary system was a fair system. Nothing has been the same since.

Since 1971, The Federal Reserve has printed money into the stratosphere, which has ballooned money supply, along with the Federal Reserves balance sheet. All you need to do to see this damage, is to observe the M2 Money Supply. For additional insight, please refer to the “WTF Happened In 1971” website (https://wtfhappenedin1971.com/).

For those unmotivated to DYOR (Do Your Own Research), here are a few charts, that I personally found to be mind-blowing charts & other relatable ones…

The rich get richer because they control most of the assets. The poor get poorer because they virtually own no assets at all. Unfortunately, while the rich thrive, poor people are just trying to survive. Owning assets (like the rich do) help offset the inflationary pressures that Quantitative Easing (QE) (aka money printing) can cause. Those who own nothing (aka “the poor”) cannot compensate for the higher prices that inflation, through money printing, will cause. This difference can cause tension. Tension as the banks & the investor class are the priority, and, “We The People” are an afterthought. This is the fundamental baseline for how the Federal Reserve was created in the first place, a beneficiary for the banking system & the elite.

On November 22nd, 1910, a secret meeting had taken place that represented (at the time) a quarter of the world’s wealth. A “boys club” known as, The Jekyll Island Club. This club had only 100 members, where prominent club members included the likes of Andrew Carnegie (Steel magnate), John D. Rockefeller (Philanthropist & the wealthiest man in the world at the time), Cornelius Vanderbilt (Railroad baron), the Warburgs of Hamburg, the Rothchilds of Paris & London, & led by the mastermind himself, J.P. Morgan (the secret father of the Federal Reserve).

Prior to the creation of the Federal Reserve, J.P. Morgan had acted in its place, saving the American economy from collapse twice in less than 15 years. These acts of “savior” innovated a blueprint for the creation of the central bank. For the Federal Reserve to function properly, the prerequisites of this bank needed to be a government institution with full backing & credit of the United States government. It must maintain its independence & be free of government oversight. The most critical component for J.P. Morgan & his “innovation” was for this central bank to remain independent. This mandate was in efforts to maintain full control (privately) of the money supply, in order to fend off takeover by politicians & government (Baratta, 2020). However, rules were meant to be broken; 1) The Great Depression (where the Fed lost independence in 1933, with the passing of the “Glass-Steagall Act & not regaining its independence until 1951 & 2) Richard M. Nixon turning money into fiat currency (by effectively taking away the beautiful relationship that money has with gold.

J.P. Morgan insisted that the central bank Federal Reserve Notes: 1) Should always be backed by gold & 2) It should equal to 40% of the currency it issued (Baratta, 2020).

For the last 53 years (1971 to 2024), money backed by nothing (or as some might argue oil, military & war), it is simply worthless. The only thing that would keep this type of worthless money in circulation is faith. Therefore, if the Federal Reserve, & other global institutions that make up the banking system, were to somehow ever make citizens lose “faith” in the currency that they “managing" would be GAME OVER for that said currency & system. The cause of death most likely will be due the DEBT & CURRENCY DEVALUATION. According to the US Debt Clock (usdebtclock.org), our debt (at least in the United States, is a nation denominated in over $35 TRILLION dollars in debt. This debt (and this is not only a US problem, but a global one), will likely NEVER be repaid.

Our current unsustainable path is being lead by mismanagement of spending (debt) & an ever-increasing balance sheet. This forcibly has led everyday citizens to constantly place their hard-earned money at risk. Risking one’s money just to have an attempt to outpace the speed inflation (a slow & silent tax that steals money from people).

In “normal” times, the Federal Reserve has a mandate of 2%. A mandate where if you just hoarded cash, & did nothing, inflation would steal 2% of your honest work from you each year (thanks to this invisible tax called “inflation”). If we are in deflationary periods, it is less than 2% stolen from you, which equates to a good thing for citizens (think increased consumption & a higher standard of living) & the environment, bad for government & business (think higher interest rates, higher unemployment & decreased production). Ultimately however, bad for everyone, as is incentivizes people to not spend money. If we are in inflationary periods it is more than 2% (good for government, & horrible for citizens). My deeper understanding of how money really works, and who it benefits, has totally shifted my way of thinking to align with the Austrian School of Economics & to be of the opinion that We, The People can do much better as a society if the Federal Reserve ceases to exist.

Conclusion:

To conclude, liquidity in financial markets is equivalent to a sugar high. The more sugar you have, the more instability (& stress) you create for yourself (& potentially others). When more money (liquidity) enters the markets, as we have recently seen to combat the COVID-19 pandemic, more buyers can enter the markets. When there are more buyers than sellers, asset values rise; when there are more sellers than buyers, asset prices drop (causing a liquidity crisis). Looking at how liquidity functions in society, I wanted to give a secondary angle on what “Monopoly money” truly looks like in visual form (see the charts below) (Baratta, 2020).

4.4x Rise - Fed: $925B (2008) to $4.1T (2020) & Dow: 6700 points to 29,500 points.

19% Drop - Fed: $4.4T (2018) to $3.6T (2020) & Dow: Drop of 19%.

11% Rise - Fed: $3.6T (2019) to $4T (2020) & Dow: Rose by 11%.

What these charts represent is how, whatever the Federal Reserve does, the stock market will exactly match it. In other words, the stock market (& all asset classes) follow the Federal Reserve balance sheet. It follows it, because the Federal Reserve controls the money. So if this is to be true (which it is), & if the Federal Reserve needs to prevent the entire financial system from collapse (which it is fighting now & is inevitable with nothing backing it but faith), then the ONLY arsenal that those with money printers have (aka governments, globally) is TO PRINT MONEY. So, as an investor, simultaneously, trying to survive & thrive, you either play their game (because you now know the rules) or you get left behind (because you grew fearful to ever play their game).

As long as you have discipline & long-term investor patience (a skill as much as an art), & observe the movement(s) of the Fed balance sheet, it’s your game to lose. The US empire is drawing to a conclusive close, as the Roman Empire did. End the Fed. The Fourth Turning is near. Don’t agree? Fine. Here is a little bonus (see chart(s) below).

And worst of all, this…

Bonus: Research for this blog post, I had curiosity to see when the WEF (World Economic Forum) was founded, & to no surprise, not only did it come from a meeting to brainstorm solutions to big challenges (much like the foundation for The Federal Reserve), but it was also founded in the infamous year of non other than 1971. January 1971 to be exact. Go figure. See for yourself…

WTF Happened in 1971?!

Is all this one giant coincidence? I beg to differ, but the verdict is still out.

📚Hand-Picked Recommendations:

#SowSaveSustain

Raven at Finperma

Source(s) Verification:

@CatalystVoices. (2021, September 29). Catalyst. Retrieved from X: https://x.com/CatalystVoices/status/1443249980525973506

@DarioCpx. (2024, August 30). JustDario. Retrieved from X: https://x.com/DarioCpx/status/1829306357130125698

@GregCrennan. (2024, August 29). Golden Coast (Cassandra). Retrieved from X: https://x.com/GregCrennan/status/1829203827683406289

Baratta, A. (2020). The Great Devaluation. Hoboken, New Jersey: John Wiley & Sons.

Dalio, R. (2022, May 02). Principles for Dealing with the Changing World Order by Ray Dalio. Retrieved from YouTube: https://www.youtube.com/watch?v=xguam0TKMw8

Mauldin, J. (2023, October 06). Mauldin Economics. Retrieved from The Big Cycle: https://www.mauldineconomics.com/frontlinethoughts/the-big-cycle

r/ABoringDystopia. (2024, April). I made a 2024 version with the most current data I could find, and also adjusted some of the 1970 prices that I found to be slightly inaccurate. Retrieved from Reddit: https://www.reddit.com/r/ABoringDystopia/comments/1c9sk2y/i_made_a_2024_version_with_the_most_current_data/

River. (2024, April 05). River Learn. Retrieved from YouTube: https://river.com/learn/terms/c/cantillon-effect/

St. Louis Fed. (2024, August 27). M2 (M2SL). Retrieved from FRED: https://fred.stlouisfed.org/series/M2SL

VantagePoint. (2024). unrealized-gains-losses-on-investment-securities2. Retrieved from VantagePoint: https://www.vantagepointsoftware.com/blog/navigating-permanent-inflation/unrealized-gains-losses-on-investment-securities2/#

Waldbillig, L. (2014, January 20). 1971 Cost Of Living. Retrieved from Historys Dumpster: https://historysdumpster.blogspot.com/2014/01/1971-cost-of-living.html

World Economic Forum. (2023, February 28). Charted: Here's how US goods and services have changed in price since 2000. Retrieved from World Economic Forum: https://www.weforum.org/agenda/2023/02/charted-heres-how-us-goods-and-services-have-changed-in-price-since-2000/

WTF Happened In 1971. (2024). WTF Happened In 1971. Retrieved from WTF Happened In 1971: https://wtfhappenedin1971.com/

Ziliak, J. P. (2014, November 28). Rural Poverty, Before and After the War. Retrieved from HAC: Housing Assistance Council: https://ruralhome.org/rvpoverty2014-ziliack/